About the Resource Library

This page contains dozens of articles on short term travel insurance that will help you quickly understand international insurance. For example, terminology, purchasing details and managing your insurance coverage are topics that are all covered within these articles. Choose an Article From the Topics Below

List of Articles

- Auto-decline conditions and insurance solutions for short-term insurance

- Benefit period determines insurance coverage

- Chart comparing evacuation benefits

- Chart comparing lost luggage benefits

- Chart comparing political evacuation benefits

- Chart comparing terrorism benefits

- Chart comparing trip interruption benefits

- Inexpensive short-term health coverage in the USA

- Making sure your short-term insurance will cover claims paid in the USA

- Pay-per-day rates for short-term plans

- Short-term insurance & the “benefit period”

- Short-term plan that covers pre-existing conditions

- Short-term plans and home country coverage

- Short-term vs long-term major medical coverage

- The beauty of short-term health plans

- The cost of not having short-term team insurance – A true story

- Trip cancellation with medical & evacuation coverage

- What to look for in short-term health insurance

Auto-decline conditions and insurance solutions for short-term insurance

All of us are aware of the difficulty of getting health insurance if we have a chronic condition. Yet many think that because their chronic condition was covered on their group health insurance plan they can get coverage on an individual plan. Underwriting is much stricter for individual plans and many chronic conditions will automatically be declined. Here is a list of auto-decline conditions if apply for a long-term international health insurance plan from a large international insurance company we work with:

AIDS/HIV, Alcohol/Drug dependence within the past 10 years, Alzheimer’s Disease, Bipoloar Disorder, Cardiomyopathy, Cerebral Palsy, Cirrhosis of Liver, Crohn’s Disease, Congestive Heart Failure, Down’s Syndrome, Hemophilia, Hepatitis C, Hodgkin’s Disease, Hydrocephalus, Infertility Treatments, Leukemia, Lou Gehrig’s Disease, Multiple Sclerosis, Muscular Dystrophy Disease, Parkinson’s Disease, Psychosis, Quadrapalegia, Schizophrenia, Scoliosis, Spina Bifida, Suicide Attempt (any history), Systemic Lupus Erythematosis, Transplants (Heart, Lung, Liver, Kidney)

But this isn’t the whole story. There are numerous 2 and 3 year plans that provide medical coverage excluding coverage for pre-existing conditions. These plans all include medical evacuation as well. So if you plan to travel overseas and presently have US insurance, keep that insurance. Then add a 2-3 year plan (which you can take out for periods as short as 3 days if you wish) which will include medical evacuation coverage and medical coverage for non pre-existing conditions

Benefit period determines insurance coverage

Often when choosing a short-term plan we only focus on the daily or monthly premium. But there are many other matters that are of vital importance. We need to ask ourselves what is the deductible? What is the maximum coverage? How is pre-existing condition defined? Is there any provision for unexpected recurrence of a pre-existing condition? Can the plan be renewed? Can it be renewed online? And another vital question is, What is the benefit period? The benefit period defines the amount of time a short-term plan covers an individual from the time of injury or sickness. If you were on a short-term plan and were injured one day before you came back to the USA and your insurance ended, would you have any coverage? On most plans you will be covered for six months from the time of injury. This is the benefit period. Also, be aware that some insurance companies scale back on maximum coverage if the benefit period is in the USA. If the plan you are choosing does not have a good benefit period, it would be wise to look at another plan. You can see a wide variety of short-term plans that we have available at https://www.gninsurance.com/group-travel/.

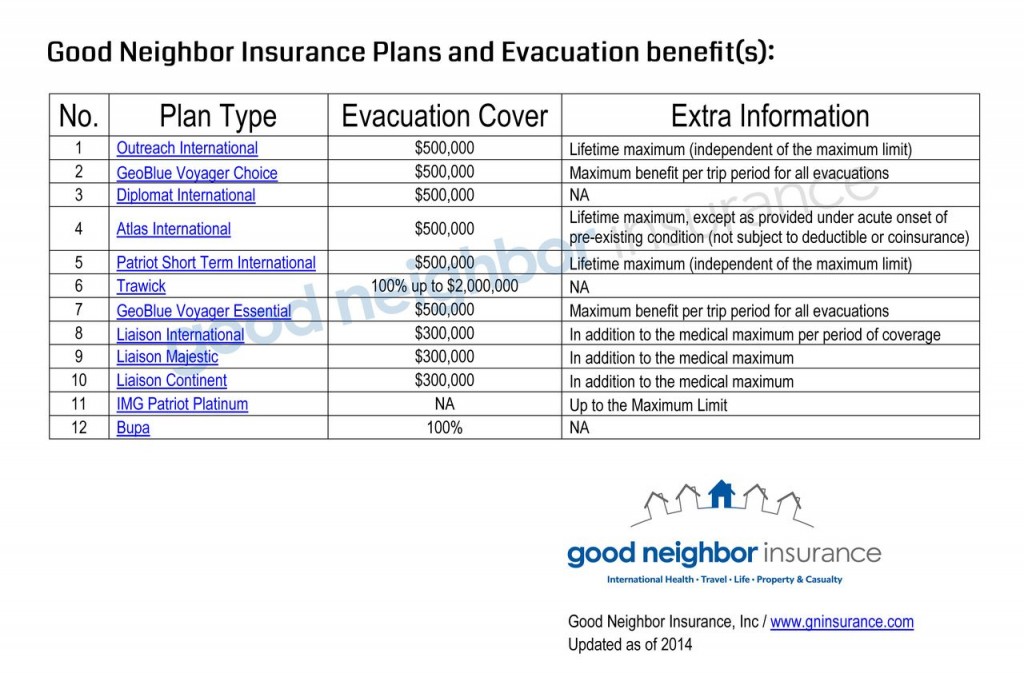

Chart comparing evacuation benefits

Evacuation Benefits and Emergency Medical Benefits Compared:

International short-term travel medical plans with an evacuation benefit

Evacuation (incl. medical evacuation) – Emergency Evacuation includes medical due to outbreaks, epidemics, threat of natural disaster, political evacuation due to civil unrest (treated separately), and emergency medical evacuation to the nearest qualified medical facility that can handle the medical condition. Includes expenses for reasonable transportation (either public transport or private as reasonable based on the condition) resulting from the evacuation; and the cost of returning to either the home country or the country where the evacuation occurred. Sometimes includes remote transportation in the event of a diagnosis of a critical medical condition which is not necessarily immediately life-threatening, but severe enough that it could result in death or a permanent disability if not treated right away. Any medical treatment (after any deductibles) are usually paid from your medical insurance benefit. May also include an Emergency Reunion Benefit, or Return of Minor Children.

(see Glossary)

When comparing short-term plans, some clients are interested in seeing what benefits each carrier has in case they might need to be medical evacuated due to emergency in the course of their travels. This is one of the greatest benefits of international insurance as evacuation or medical evacuation costs can reach $25,000-175,000. based on the nature of the emergency. Some plans pay medical costs incurred as part of the evacuation, others allow medical evacuation benefit limits to be the same as the maximum policy amount

If you are worried about emergency evacuation due to where you plan to travel, we’d recommend our Trawick Safe Travels plan. If you’d like having stronger medical coverage and benefits in addition to evacuation, check out our IMG Patriot Platinum Plan.

NOTE: The attached .pdf (click on the chart) has active links you can follow directly to the plans listed here.

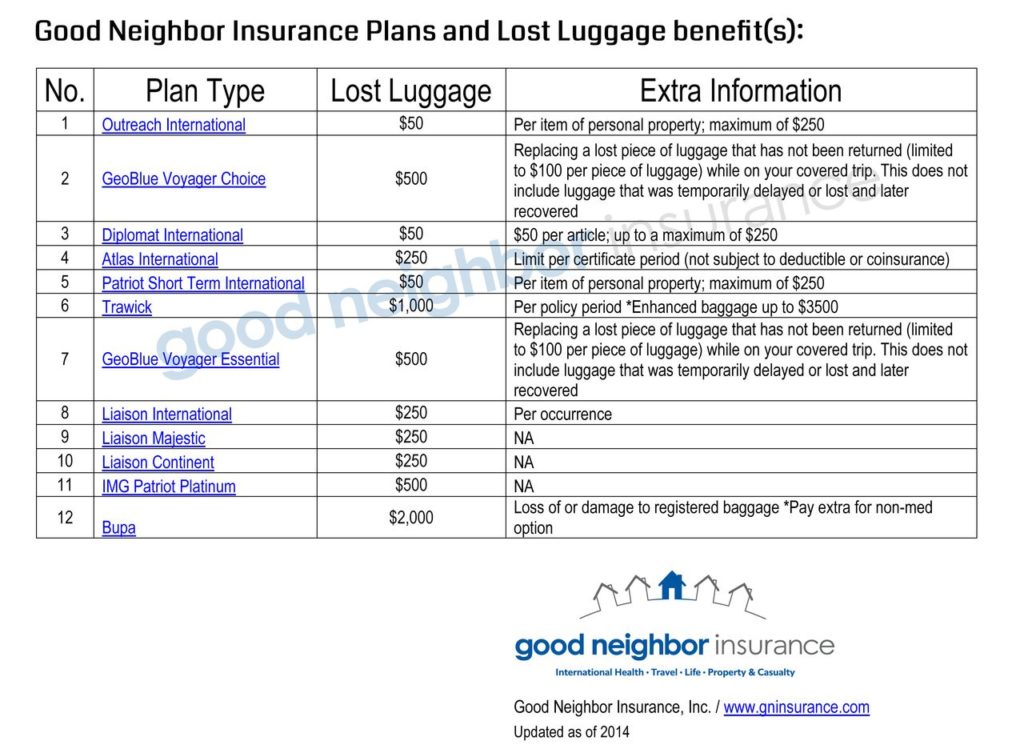

Chart comparing lost luggage benefits

Lost Luggage Benefits Compared:

International short-term travel medical plans with a lost luggage benefit

Lost Luggage (Loss/Theft) – Due to damage to, or loss of, or theft of your checked or stored baggage or personal items by a common carrier, or while stored with your hotel. It will also usually include coverage for the replacement costs of travel documents, and sometimes bag tracking.

(see Glossary)

When comparing short-term plans, some clients are interested in seeing what benefits each carrier has in case they might need to replace lost or stolen property in the course of their travels. Depending on the plan, this can vary greatly.

If you are worried about theft or loss due to where you plan to travel we’d recommend our Trawick Safe Travels plan. They also have a rider to up the limit for more expensive equipment you may be taking with you. If you’d like having stronger medical coverage and benefits in addition to lost luggage, check out our IMG Patriot Platinum Plan.

NOTE: The attached .pdf (click on the chart) has active links you can follow directly to the plans listed here.

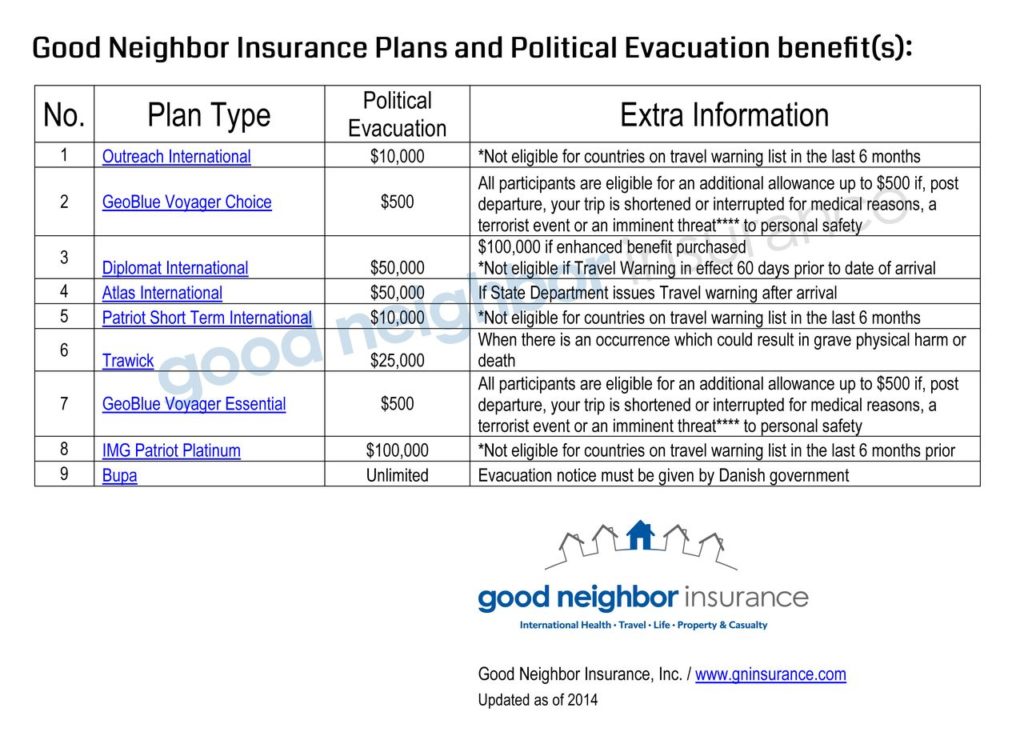

Chart comparing political evacuation benefits

Political Evacuation Benefits Compared:

International short-term travel medical plans with political evacuation benefits

Political Evacuation – Often lumped together with non-medical or security evacuations, political evacuations are for situations where one fonds themselves either trapped or expelled or at bodily risk due to civil uprisings, riots, military coups, political unrest, or being identified as a “persona non grata” or being forcibly expelled from the country you are visiting. Security evacuations are different from political evacuations. Unlike a security evacuation (necessary for impending natural disasters, etc.),…a political evacuation is for situations of political instability, civil unrest, or military action.

(see Glossary)

When comparing short-term plans, some clients are interested in seeing what benefits each carrier has in case they might need to be political evacuated due to instability of their destination, etc. Depending on the plan this can vary greatly. Most plans will deny benefits if the USA or British Foreign office has issued a State Department travel warning prior to your departure and within 6 months of your travel dates. This benefit will usually also not cover you in the event that an advisory to leave a certain country or location is issued by the United States government after the insured person’s arrival date, and the insured person unreasonably fails or refuses to to heed such warning or depart the country or location.

If you are considering political evacuation due to travel to a country where you might be at risk, we’d recommend our Diplomat International plan. If you’d like having stronger medical coverage and benefits in addition to political evacuation, check out our IMG Patriot Platinum Plan.

NOTE: The attached .pdf (click on the chart) has active links you can follow directly to the plans listed here.

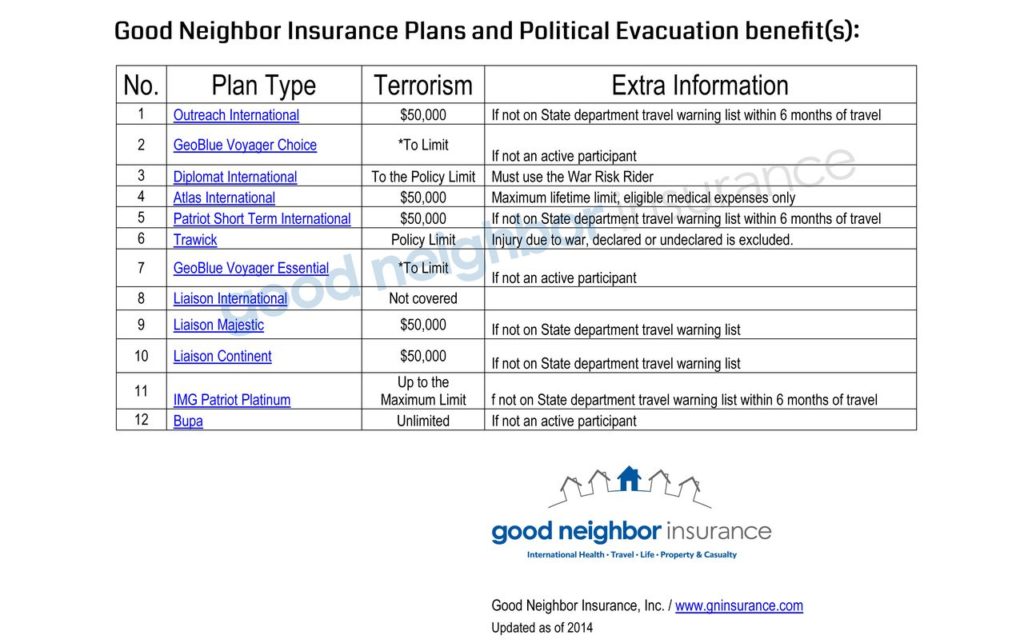

Chart comparing terrorism benefits

Terrorism Benefit(s) Compared:

International short-term travel medical plans with a stated terrorism benefit

Terrorism – includes criminal acts, including against civilians, committed with the intent to cause death or serious bodily injury, or taking of hostages, with the purpose to provide a state of terror in the general public or in a group of persons or particular persons, intimidate a population, or compel a government of international organization to do or to abstain from doing an act.

(see Glossary)

When comparing Short-term plans, some clients are interested in seeing what benefits each carrier has in case of terrorist attack in terms of political evacuation, etc. Depending on the plan this may vary. Most plans will deny benefits if the USA or British Foreign office has issued a State Department travel warning prior to your departure or within 6 months of your travel dates. This benefit will usually also not cover an act of terrorism in the event that an advisory to leave a certain country or location is issued by the United States government after the insured person’s arrival date, and the insured person unreasonably fails or refuses to to heed such warning or depart the country or location.

For terrorism and countries where you might be at risk, we’d like to recommend our Diplomat International plan here (not listed on chart): https://www.gninsurance.com/travel/terrorism/diplomat-international/ If you’d like not only a terrorism benefit up to the max policy amount, but also stronger medical coverage in addition to higher limits across the board, check out our IMG Patriot Platinum Plan.

NOTE: The attached .pdf (click on the chart) has active links you can follow directly to the plans listed here.

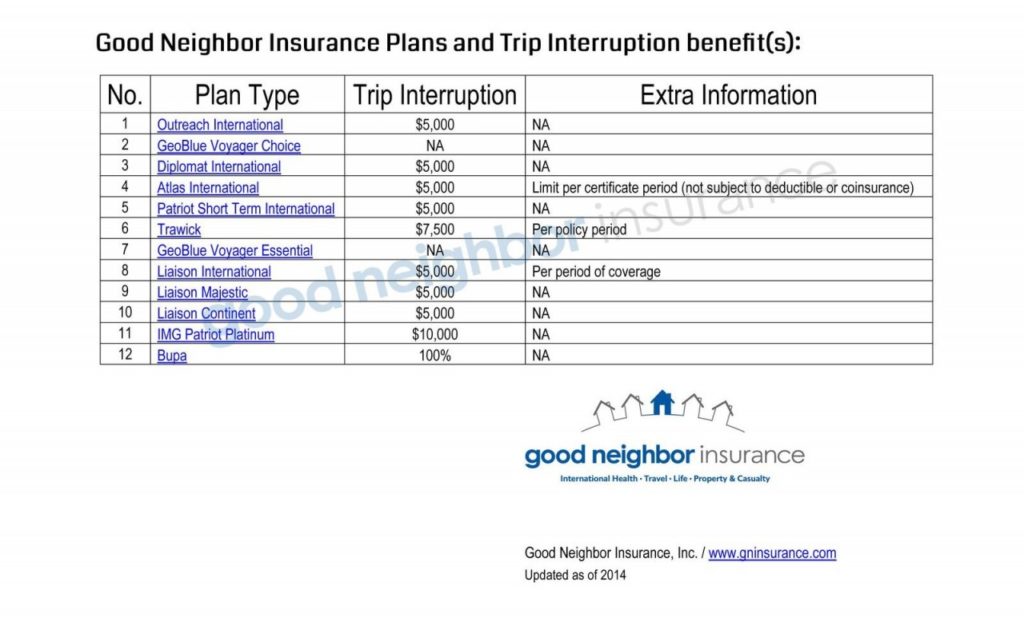

Chart comparing trip interruption benefits

Trip Interruption Benefits Compared:

International short-term travel medical plans with a trip interruption benefit

Trip Interruption – Trip interruption plans typically reimburse you for pre-paid non-refundable travel expenses if an unexpected crises (e.g., death of a family member, sickness, airline strike, travel supplier bankruptcy, among other crises) occurs during your trip causing it to be cancelled, interrupted or delayed.

(see Glossary)

When comparing Short-term plans, some clients are interested in seeing what benefits each carrier has for Trip Interruption. Depending on the cost of your trip (expenses) this may cover all or a portion of your overall trip expenses.

As you can see, if you think you need a plan with higher trip interruption benefit, consider the Trawick Safe Travels plan. If you’d like not only a higher trip interruption benefit but also stronger medical coverage in addition to higher limits across the board, check out our IMG Patriot Platinum Plan.

NOTE: The attached .pdf (click on the chart) has active links you can follow directly to the plans listed here.

Inexpensive short-term health coverage in the USA

With a tight budget, a short-term major medical plan might be your best short-term option for health insurance. Good Neighbor Insurance has a plan with a “No Decline Question.” Almost all plans like this ask, “Have you been declined insurance?”If you answer yes, you cannot enroll. (The change has not been made yet on the online ap. So be assured that if you answer “yes” to the decline question the application will still go through.) This plan has a $50 deductible at urgent care facilities and 80%/20% co-insurance to $5,000 (not $10,000). No Social Security number is required. All legal U.S. residents can apply. The plan is underwritten by an A+ Superior rated carrier that has almost $9 billion in assets. In most states, a full 12 month plan is available. The plan is available in all states but the following: CT, GA, KS, MD, MA, MN, MT, NJ, NY, ND, VT and WA

This is good, inexpensive coverage before you leave the USA for an overseas posting. Or do you need coverage during a short or long furlough in the USA? Do you need coverage for a child attending college in the USA? Do you need coverage while looking for a job that provides health insurance? Or maybe the cost of a long-term major medical plan is out of your reach right now. In any of these cases the “HCC Life STM” formerly “Amigo” will work for you. If you can say “no” to five questions, the most difficult one being listed below, you can apply for this coverage. Here is Question 3 on the online application:

Within the last 5 years has any applicant been diagnosed, treated, or taken medication for or experienced signs or symptoms of any of the following: cancer or tumor, stroke, heart disease including heart attack, chest pain or had heart surgery, COPD (chronic obstructive pulmonary disease) or emphysema, Crohn’s disease, liver disorder, degenerative disc disease or herniation/bulge, rheumatoid arthritis, kidney disorder, diabetes, degenerative joint disease of the knee, alcohol abuse or chemical dependency, or any neurological disorder?

The per-month cost for a 24 year old male with a $500 deductible plan is $73.24. .

Making sure your short-term insurance will cover claims paid in the USA

To utilize your international insurance coverage, medical care must be initiated outside the USA. What does this mean? When you develop a medical condition as a short-term worker while on a team or while on individual short-term insurance, if you do not see a doctor while outside the USA, you will not be covered for added medical care back in the USA.

Here is the procedure you must follow:

- If the condition is not an emergency, call the ?Call Collect? number on your medical ID card and consult with the insurance company concerning your medical condition. NOTE: If it is an emergency, go immediately to the hospital or see a doctor and call the insurance company later

- Visit the doctor or medical facility

- Pay the medical facility for medical care received. Make sure you get a receipt and also a detailed explanation of all care received–both in the hospital and at the doctor’s office

- Get a dated written statement from the doctor explaining your medical condition and what you were treated for

- Submit these documents as soon as possible to the insurance company–no later than 90 days from the initial medical treatment

- When you pursue further medical treatment in the USA, consult with the insurance company to make sure you are using a doctor in its network

If you fail to initiate medical care outside the USA and then ask the insurance company to reimburse you for medical expenses for care received within the USA, the insurance company will not cover those claims. Why do they do this? Because this is the only way they can be sure that the medical condition developed while you were outside the USA. The whole purpose of international health insurance is to protect you while outside the USA.

Pay-per-day rates for short-term plans

In the past when you applied for a short-term insurance plan and needed coverage for 20 days, you would pay for a full month of insurance. Or if you were going to be gone for 35 days, you would pay for one and a half months insurance. Now two major companies permit you to purchase insurance for the exact amount of days you will be gone with a minimum purchase of seven or ten days, depending on the company. When you apply for these plans online, they ask for the day you want the insurance to be effective and the day you want it to expire. Premium calculations are based on the total number of days involved. You can compare short-term plans where you would pay-per-day by going to https://www.gninsurance.com/group-travel/. Both of these plans are very cost-effective. The total premium for $50,000 maximum coverage ($250 deductible) for two weeks for someone 29 and under can be less than $15.00.

Short-term insurance & the “benefit period”

Not all short-term plans are equal–so be careful. One thing to study closely is the “Benefit Period,”–the length of time medical care is extended after an injury or sickness. Here is the problem: You are insured for a two-week trip. During the last day for your trip you break your ankle. Your insurance coverage expires the next day. But what about the broken ankle? Most short-term plans provide a six-month “Benefit Period” from the time of the accident. But there are still things to watch for: Will they give you complete coverage for your plan if medical care is received in the USA and not overseas? Do they require you to seek help outside the USA first? Do they limit coverage if medical care is received in the USA? And do they offer a six-month benefit period? We do have some good short-term plans with six month benefit periods.

Short-term plan that covers pre-existing conditions

Good Neighbor Insurance now offers a short-term health insurance plan for international workers that will provide $2,500 in coverage for pre-existing conditions if the care is received outside the USA. You may be aware that short-term plans traditionally give absolutely no coverage for pre-existing conditions. This plan, although short-term, is renewable up to three years. What’s more, it offers $100,000 of medical evacuation insurance, and overall the rates are lower than all the other short-term international health insurance plans. If you are interested in a short-term plan that at least gives limited coverage for pre-existing conditions, please let us know. We will be happy to e-mail and/or mail it to you. You can also apply for this plan (Liaison International) online at www.overseashealthinsurance.com.

Short-term plans and home country coverage

Short-term international health plans focus on providing international health coverage outside the USA. Yet some of them do provide limited coverage in the USA. For example, here is a quote for home country coverage from the brochure of one popular plan: Incidental Home Country Coverage: During the Period of Coverage an insured person may return to their country of residence for incidental visits up to a cumulative two weeks total, subject to:

- The insured person must have left their country of residence

- The total Period of Coverage must be for a minimum of 30 days

- The return to the country of residence may not be taken to receive treatment for an illness or injury incurred while traveling

Most short-term plans provide some coverage for incidental trips to the Home Country while the insured is on an international trip. In most of these cases such as coming home for a wedding, if an insured needs medical care for non-preexisting conditions, all will be covered, including medications, after the deductible has been met. Thus if the individual has a $100 deductible and needs to go to the doctor for bronchitis, everything after the deductible will be covered by the insurance. Of course, medical charges will be subject to co-insurance limits.

When purchasing international short-term health insurance, it is important to remember that this insurance is not meant for coverage in the USA. In most cases, the coverage stops the minute an insured resident of the USA arrives back in the USA. The insurance is meant to be a supplement to a person’s domestic insurance and only provide coverage while outside the USA–something that is not generally provided by domestic health plans.

The “Benefit Period” is the length of time a person will be cared for under a plan if they have an injury. If an individual takes out ten days of coverage for a trip to Mexico, and then breaks a leg on the ninth day, does that mean there will be no coverage for the broken leg after ten days” Generally, insurance companies will pay claims for the broken leg for up to six months from the time of injury. The six months is called the “Benefit Period.”

Sometimes insurance companies will limit both the time of the Benefit Period, and they will also cap reimbursement for medical care received in the USA during the Benefit Period. This is a very important part of short-term coverage, so ask your insurance broker about the Benefit Period when you purchase short-term insurance.

Short-term vs long-term major medical coverage

If you are going to be involved in overseas work for longer than three years, we would advise you to get long-term major medical insurance. Here is the problem: Short-term major medical can cover you up to three years, but then the plan will have to be re-written. If, during those first three years, you become sick, e.g., hepatitis, diabetes, urinary tract infection, back problem, etc. these will all be considered “pre-conditions” and will not be covered when you apply for the next short-term plan. That is not the case with the long-term policies. The long-term policies will cover you for the rest of your life as long as you meet the residency conditions and keep your account current. Some folks opt for the short-term major medical coverage because it is less expensive, but this is taking a major risk if you are a career worker. Also, with a career plan you get at least six months of coverage in your home country in any given year. That is a good time to get medical needs taken care of. Short-term plans do not give you a similar benefit. If you have questions about the wisdom of choosing a long-term or short-term plan, please contact us.

The beauty of short-term health plans

Is any insurance plan beautiful? Probably not! But short-term health plans do have some advantages. Along with the medical coverage, you can get coverage for:

- The exact number of days you are outside your home country

- No underwriting questions

- A wide selection of deductibles and maximum coverage options

- Apply and renew your policy online

- All policies include medical evacuation and some term life or AD&D

When applying online, you will get your Medical ID Card e-mailed to you almost immediately–sometimes within 30 seconds of submitting your application. And overall the cost of short-term health coverage is low. A person aged 19-29 can purchase $50,000 of coverage with a $250 deductible for as low as $1.00 a day.

Some things to keep in mind:

- International short-term health coverage will not cover pre-existing conditions and maternity

- If you do not have proof that you first received medical care while outside the USA, the insurance company will not reimburse you for follow-up care in the USA

If you want to get an overview of a wide variety of international short-term health plans, please go to https://www.gninsurance.com/group-travel/.

The cost of not having short-term team insurance – A true story

Don Jenkins, on his third mission trip to Central America, spent the day laying blocks for a church camp in La Fortuna, Costa Rica. That night he tripped on a concrete asphalt trench and hit his head. Jenkins suffered a subdura hematoma, and was in a coma for 30 days. He underwent two brain surgeries and was hospitalized for 90 days–6 in San Jose, Costa Rica, and 74 in his hometown. While still in a coma, he was flown home.

The fall would wind up costing his family more than $90,000. Because the accident occurred outside the United States, Jenkins’ domestic health insurance wouldn’t pay. Family members did not have the money, so his daughter mortgaged her house to get the $30,000 needed for an air ambulance to return Jenkins to Kentucky. The hospital in Costa Rica wouldn’t release Jenkins until the hospital bill was paid. His son used his corporate credit to pay the $22,000 bill, which the family is now repaying in installments. The doctors and surgeons in Costa Rica agreed to accept monthly payments. With donations from churches, friends, family members, and the Kentucky United Methodist Conference, about half of the $90,0000 has been paid. Now Mr. Jenkins’ family is on their own mission–to tell everyone to check their domestic health insurance before leaving the United States. Some policies cover health care in another country. Some don’t. Even if a policy will pay for treatment, generally it doesn’t include medical evacuation. (By Alberta Lindsey, Times-Dispatch Staff Writer, May 5, 2001, (condensed by J. Gulleson)

Trip cancellation with medical & evacuation coverage

In most cases airlines will not reimburse unused tickets. Because of this, many individuals are purchasing Trip Cancellation coverage that also includes medical and medical evacuation coverage. Trip Cancellation rates are based on the dollar amount of the ticket and/or any money that will be lost if the trip is cancelled, as well as the age of the insured. Generally, such plans also include coverage for trip delay, lost luggage, return of mortal remains, etc. We have a person who is under 50 years old who is purchasing a ticket for $600 and paying $61 for the coverage. Therefore, he has full medical evacuation coverage, medical coverage up to $100,000, and he will be reimbursed $600 if his trip is cancelled. For a Trip Cancellation quote, go to www.overseashealthinsurance.com.

There is also the possibility of insuring teams on a Trip Cancellation with Medical/Medical Evacuation plan. If you are interested in this kind of team coverage and/or individual coverage, please contact GNI.

What to look for in short-term health insurance

With a casual glance all short-term health insurance plans look the same, but there are important differences. Varying rates (premiums) are not the only thing to keep in mind. First, when comparing premiums on different plans make sure the maximum coverage and deductible you are considering are the same amounts for each plan. For example, compare the rates for a maximum coverage of $50,000 with a $250 deductible.

After that is done, you need to ask yourself the following questions: Is home country coverage offered? How much time is allowed in the home country? Is home country coverage built into the rates or is it surcharged? What is the maximum medical evacuation amount? Is the medical coverage only for accidents or for both accidents and sickness? What is the benefit period (the length of coverage from the time the person requires medical care)? The best companies give at least a six-month benefit period. Is hazardous sports coverage offered? And if so, what is the surcharge? Although short-termplans do not cover pre-existing conditions, is there any coverage for an ?unexpected recurrence? of a former medical condition? What is the optional length of the policy: one year, two years, three years? The longer a short-term policy can be in effect, the better.