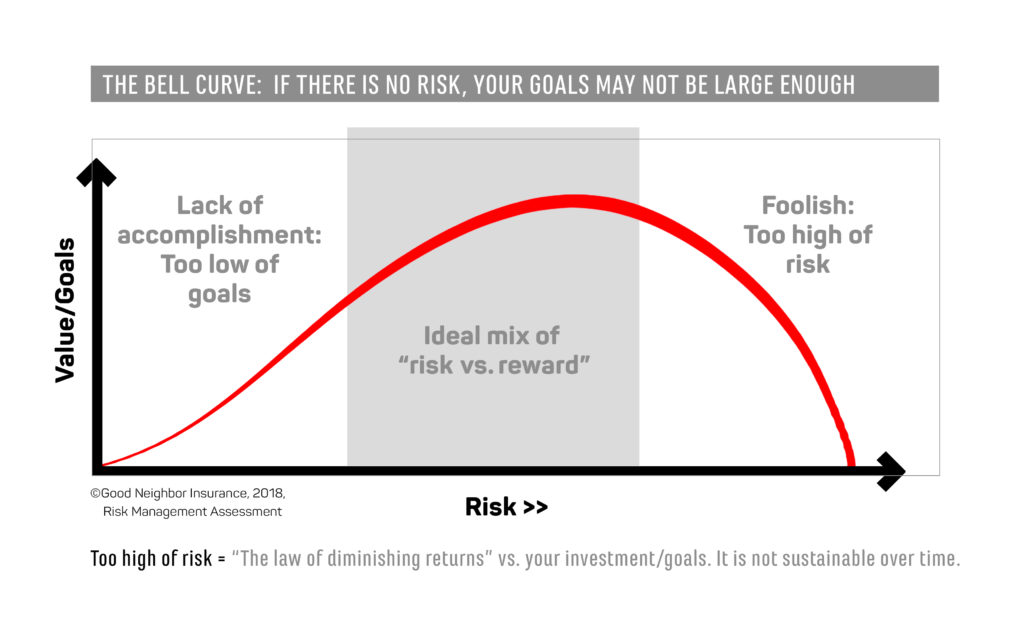

Risk Management is critical because risk is inherent to achieving any goal. Instead of trying to eliminate risk or seeking to avoid it, you should be planning and managing risk, even leveraging it, because risk = opportunity

Below are some forms of insurances/protections to share risk/spread risk so that you do not face those risks alone. (Sometimes also called “supplemental insurance” meaning in addition to international health insurance.)

Risk Management

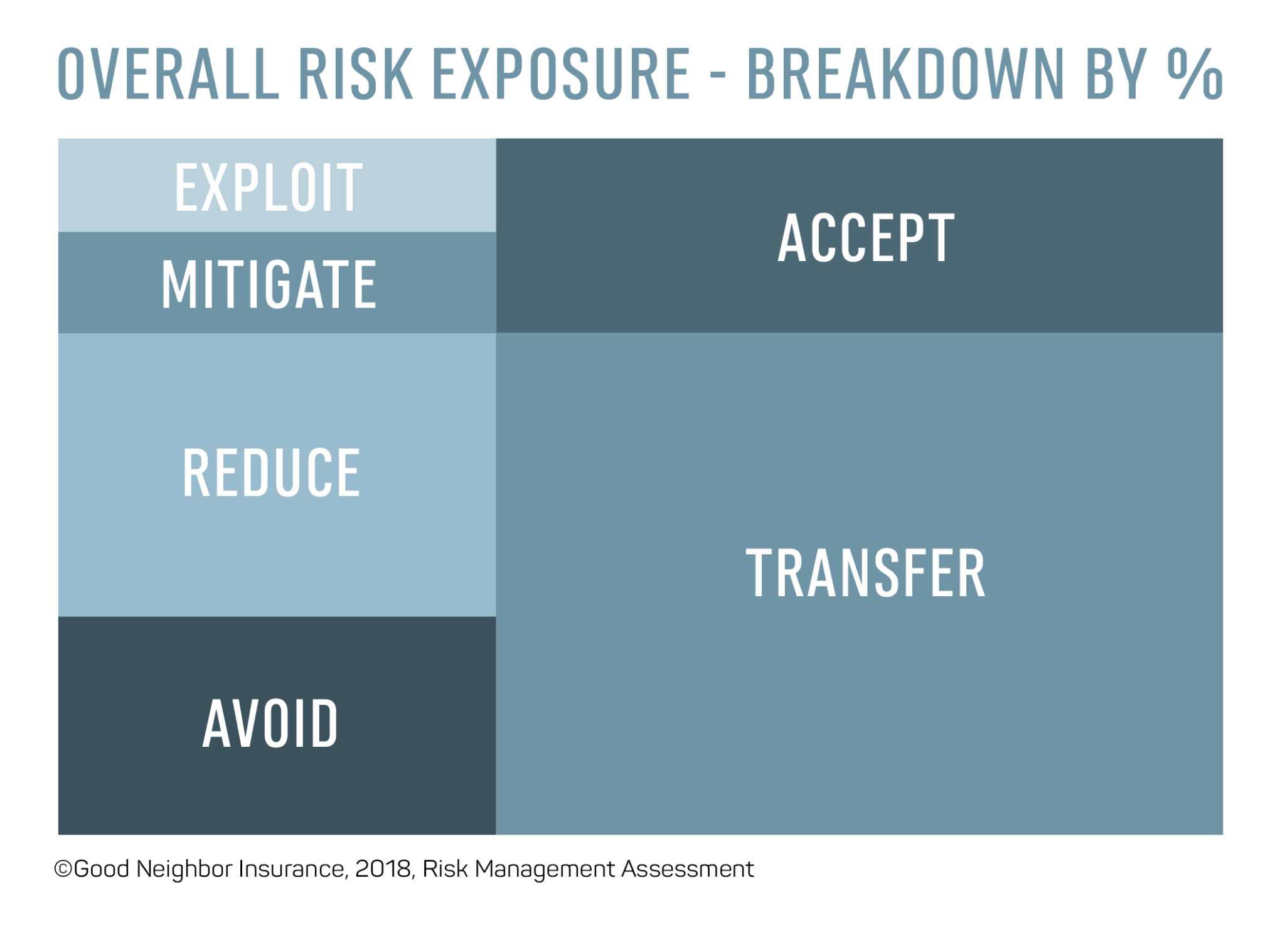

Consider the amount of risk to your organization or family and what to do with it. Consider the various types of risk you face as a family so that you control the amount of risk and choice of risks—no more, no less—that allow you to effectively pursue your personal, life, and organizational goals without failure, if one of those risks were to happen.

Includes avoid, accept, reduce, or share/transfer

Everyone is different and each organization is different in their approach to risk This should be based on your individual judgement, willingness to accept potential consequences, organizational culture, and operating style. Some might be more “risk adverse” while others by necessity or choice might be more “risk-taking.” (Some of our individual clients and groups could not do the work they are doing if they were “risk adverse.”)

Sharing risk might mean

Sharing risk might mean

- Insurance(s) or outsourcing based on the decision to share risk through insurance, hiring professional services, and other forms of contracting.

- Internal financing of risk is accomplished through the organization’s (or families) own financial resources, e.g., various forms of self-funded health plans, insurance deductibles or using your savings/reserves/credit.

- Many risks are financed internally, but many are not understood or identified beforehand.

You retain all of the risk (financial and otherwise) until you do something to address them. Unplanned retention of risk is not “risk management.” - Insurance that protects the enterprise or family from catastrophic events is often inexpensive relative to the potential loss, and the decision to transfer risk via insurance is usually common sense. Who wants to explain to a board or your supporters/donors that a $5 million loss could have been insured for $2,000? Or that a liability policy, costing a couple hundred dollars, could have covered a scam lawsuit that is now risking your entire work in a particular country and costing your hundreds of hours and bribes and hiring/dealing with local laws and legal representation?

QUESTIONS:

- Is it reasonable to avoid some of the risks (and still accomplish your goals)?

- What risks are you prepared to accept?

- What risks can be reduced by behavior/location/preparedness?

- What risks can be shared/transferred to an insurance carrier?

- Are there risks are you unwilling to address/face at this time?

Risk Identification

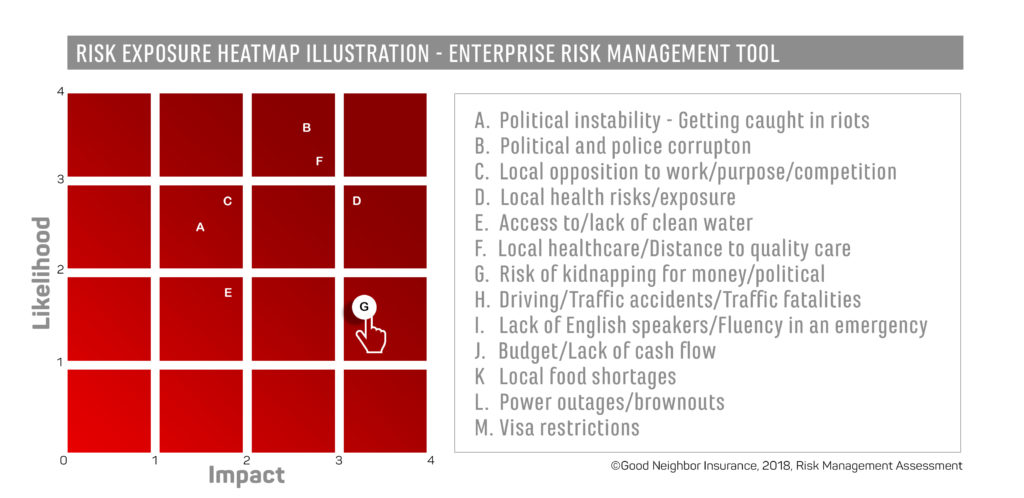

Assessing risks consists of assigning a value to each risk (or opportunity) using a defined criteria.

Refers to the extent to which a risk event might affect your family or whole organization/purpose.

Could a lawsuit cause your organization to shut down? Huge unexpected bills cause you to have to return home? A self-funded health plan may not be prepared to handle a long-term illness, such as a ”million-dollar baby” or dealing with a second crisis while already managing a large long-term crisis. Some risks may impact the enterprise financially while other risks may have a greater impact on your reputation, or the health and safety of your workers/family.